In the ever-evolving landscape of personal finance, one savings option has been gaining significant traction – the high-yield savings account (HYSA).

These deposit accounts, typically offered by online banks and credit unions, provide interest rates that far exceed the national average for traditional savings accounts.

If you’re looking to maximize the growth of your hard-earned money, understanding the ins and outs of high-yield savings accounts is crucial.

Key Takeaways:

- High-yield savings accounts offer significantly higher interest rates than traditional savings accounts, allowing your money to grow at a faster pace.

- The APY (annual percentage yield) on high-yield accounts can fluctuate based on changes to the Federal Reserve’s benchmark interest rate.

- High-yield savings accounts provide easy access to your funds, with the ability to make regular deposits and withdrawals, though there may be limits on the number of withdrawals per month.

- While high-yield savings accounts are a safer option compared to investment accounts, they have limited growth potential and may not be the best choice for long-term financial goals like retirement savings.

- When choosing a high-yield savings account, consider the interest rate, fees, minimum balance requirements, and other key features to find the best fit for your needs.

What is a High-Yield Savings Account?

A high-yield savings account is a deposit account that offers a much higher interest rate than a traditional savings account found at brick-and-mortar banks. These accounts are designed to help your money grow at a faster pace, with interest rates that can be several times higher than the national average.

1. How They Differ from Traditional Savings Accounts

The primary distinction between high-yield savings accounts and traditional savings accounts lies in the interest rates they offer. High-yield accounts typically pay a significantly higher annual percentage yield (APY), which is the amount of interest your account will accrue in a year. This means your money will grow faster in a high-yield account compared to a traditional savings account.

Apart from the higher interest rate, high-yield savings accounts function similarly to other savings accounts. You deposit money into the account, and the bank pays you interest in return. You can also make withdrawals as needed, though your bank may charge a fee if you exceed a certain number of withdrawals per month.

2. Why High-Yield Savings Accounts Are Becoming Increasingly Popular

The primary appeal of high-yield savings accounts is their ability to offer much higher returns than traditional savings accounts. With the current low-interest-rate environment, high-yield accounts provide a way for individuals to grow their savings at a faster pace, helping them reach their financial goals more quickly.

Additionally, the convenience and accessibility of these accounts, often offered by online institutions, have contributed to their growing popularity. Many high-yield savings accounts are fee-free, have low or no balance requirements, and even provide ATM cards, making them an attractive option for savers.

How High-Yield Savings Accounts Work

1. Mechanics of Interest

- APY (Annual Percentage Yield) Explained

The APY is the amount of interest your high-yield savings account will accrue in a year. This includes the effect of compounding, which can occur daily or monthly, depending on the specific account. The higher the APY, the faster your money will grow. - How APY Is Influenced by the Federal Reserve’s Interest Rate Changes

The APY for any savings vehicle, including high-yield savings accounts, can fluctuate based on changes to the Federal Reserve’s benchmark interest rate. When the Fed raises its interest rates, it typically leads to higher APYs on high-yield savings accounts. Conversely, when the Fed lowers rates, the APYs on these accounts may decrease.

2. Account Features

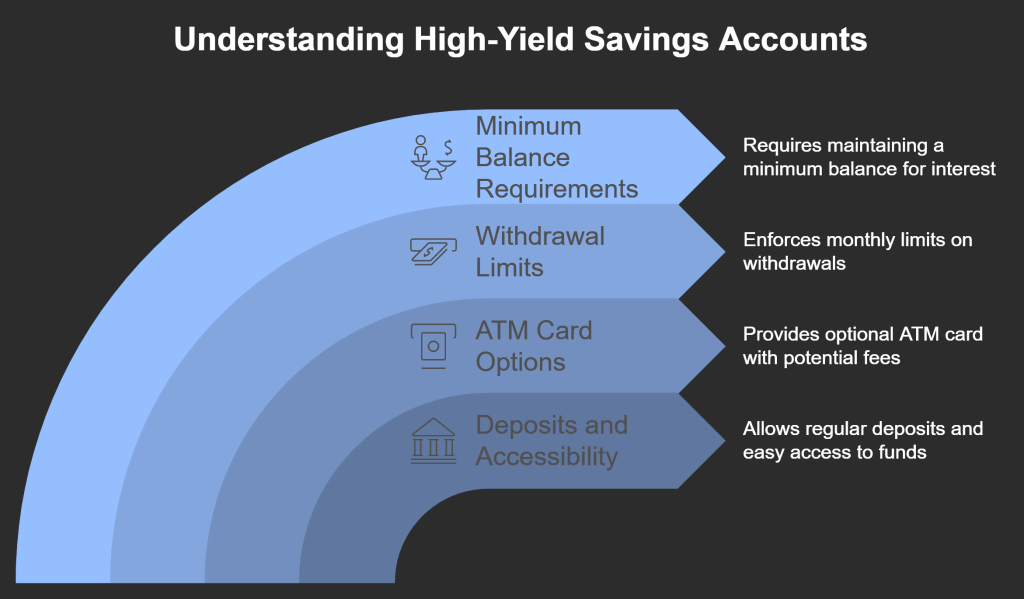

- Deposits and Accessibility

High-yield savings accounts allow you to make regular deposits and provide easy access to your money through withdrawals or transfers to linked bank accounts. This flexibility can be particularly beneficial for building emergency funds or saving for short-term goals. - Potential for ATM Cards and Associated Fees

Some online banks offering high-yield savings accounts may provide optional access to an ATM card. However, the number of transactions or amounts you can withdraw may be limited, and there may be associated fees. It’s essential to review the account’s terms and conditions to understand the specific ATM card policies. - Withdrawal Limits

Savings accounts, including high-yield savings accounts, may be subject to monthly withdrawal limits. Banks can cap the number of withdrawals you’re allowed to make in a month and can charge excess withdrawal fees. Even high-yield savings accounts that don’t limit the amount you can transfer or withdraw from your account may cap the number of times you can do it per cycle. Most HYSAs limit withdrawals to six per month. - Minimum Balance Requirements and Their Impact on APY

Some high-yield savings accounts require a minimum balance to earn the advertised interest rate. This means that if your account balance falls below the minimum, you may earn a lower APY or even no interest at all. Be sure to read the account’s terms and conditions carefully to understand the minimum balance requirements.

Benefits of High-Yield Savings Accounts

1. Financial Advantages

- Higher Returns Compared to Traditional Savings Accounts

The primary benefit of a high-yield savings account is the significantly higher interest rate it offers compared to a traditional savings account. With APYs that can easily outpace the national average, your money will grow at a much faster pace in a high-yield account. This can be especially advantageous if you’re saving for a specific goal, building an emergency fund, or simply wanting to maximize the growth of your savings. - Combating Inflation With Better Returns

Traditional savings accounts often have low interest rates, making it challenging for your money to keep up with inflation. High-yield savings accounts provide a better chance of your savings maintaining their purchasing power over time, as the higher interest rates can help offset the effects of inflation.

2. Convenience and Security

- Easy Access to Funds Compared to Investment Options

Unlike certificates of deposit (CDs), which lock your money in for a fixed term, high-yield savings accounts allow you to withdraw and transfer funds without penalty. This can be helpful if you need to access your savings for an unexpected expense or if you’re nervous about locking your money away for an extended period. - Safety of FDIC or NCUA Insurance

Funds held in high-yield savings accounts are protected by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA), up to the legal limits. This means your money is secure, even if the financial institution were to fail. - Often Have Low or No Fees

High-yield savings accounts typically come with fewer fees than traditional savings accounts. Many online banks that offer these accounts do not charge monthly maintenance fees or have low or no minimum balance requirements. This can help you maximize the returns on your savings by avoiding fees that can eat into your earnings.

Drawbacks to Consider

1. Factors That May Impact Returns

2. Account Restrictions and Fees

3. Accessibility

- The Majority of HYSAs Are Offered by Online Institutions

High-yield savings accounts are primarily offered by online banks, credit unions, and fintech companies, rather than traditional brick-and-mortar banks. This may be a drawback for those who prefer the in-person banking experience or have limited access to the internet or online banking platforms.

What to Look for in a High-Yield Savings Account

When choosing a high-yield savings account, there are several key features to consider:

| Feature | Description |

|---|---|

| Interest Rate (APY) | Compare the account’s APY to the national average to ensure you’re getting a competitive rate. |

| Compounding Frequency | Look for accounts that compound interest daily or monthly, as this can significantly impact your earnings over time. |

| Fees | Check for any monthly maintenance fees, minimum balance requirements, or excessive withdrawal fees. |

| Minimum Deposit and Balance | Understand the minimum deposit needed to open the account and the minimum balance required to earn the advertised APY. |

| FDIC or NCUA Insurance | Ensure the account is insured for up to the legal limit, providing additional security for your funds. |

| Withdrawal and Transfer Limitations | Review the account’s policies on the number of withdrawals and transfers allowed per month. |

| Additional Products | Consider whether the bank offers other financial products, such as checking accounts or investment options, that you may need in the future. |

By carefully evaluating these features, you can choose a high-yield savings account that best aligns with your financial needs and goals.

How to Open a High-Yield Savings Account

1. Research and Application Process

- Compare Different Banks and Their Offerings

Start by researching and comparing the high-yield savings accounts offered by various online banks, credit unions, and fintech companies. Consider the key features mentioned in the previous section, such as interest rates, fees, and account requirements, to find the best fit. - Gather Necessary Documents (ID, Social Security Number, etc.)

To open a new high-yield savings account, you’ll need to provide the bank with some personal information, including your: - Name

- Address

- Email address

- Phone number

- Date of birth

- Social Security number

- Apply Online or In Person

The process of opening a high-yield savings account is typically straightforward. You can complete the application process entirely online, as most high-yield accounts are offered by digital-only institutions. If you prefer an in-person experience, you may be able to open an account at a local credit union or community bank that offers high-yield savings options.

2. Funding and Account Management

- Funding the Account via Transfer or Direct Deposit

Once you’ve opened your high-yield savings account, you’ll need to fund it. This can be done by linking an existing bank account and transferring money, or by setting up direct deposit from your employer. - Setting up Automated Transfers for Regular Savings

To maximize the growth of your savings, consider setting up automatic transfers from your checking account or your employer’s direct deposit program into your high-yield savings account. This “set it and forget it” approach can help you build your savings consistently over time. - Utilizing Online and Mobile Banking Features

Many high-yield savings accounts offer robust online and mobile banking capabilities, allowing you to manage your account, monitor your balance, and make transfers with ease. Take advantage of these digital tools to stay on top of your savings.

Alternatives to High-Yield Savings Accounts

While high-yield savings accounts offer an attractive way to grow your money, they are not the only savings option available. It’s essential to consider the following alternatives as well:

1. Money Market Accounts

Money market accounts are similar to high-yield savings accounts in that they provide a higher interest rate than traditional savings accounts. However, they often come with additional features, such as the ability to write checks or make purchases with a debit card. The decision between a money market account and a high-yield savings account will depend on your specific needs and preferences.

2. Certificates of Deposit (CDs)

CDs, or fixed deposits, typically offer higher interest rates than high-yield savings accounts, but they come with the trade-off of locking your money in for a fixed term, usually ranging from a few months to several years. If you have a specific financial goal with a known timeline, a CD may be a suitable option, but be aware of the penalties for early withdrawal.

3. Cash Management Accounts

Cash management accounts are often associated with brokerage accounts and are designed to hold the money you plan to invest or use for other financial purposes. These accounts can combine the features of both checking and savings accounts, including the potential to earn competitive interest rates.

4. Investment Accounts

For those with a longer time horizon and a higher risk tolerance, investment accounts, such as brokerage accounts or retirement accounts, may provide the potential for greater returns than high-yield savings accounts. However, these accounts also carry higher risks, making them less suitable for short-term savings or emergency funds.

Conclusion

High-yield savings accounts offer a compelling way to grow your money at a much faster pace than traditional savings accounts. By understanding the benefits, drawbacks, and key features of these accounts, you can make an informed decision and choose the one that best aligns with your financial goals and savings needs.

Remember to compare the interest rates, fees, and account requirements of different high-yield savings options to find the one that will help you maximize the growth of your hard-earned savings.

With the right high-yield savings account, you can take a significant step towards achieving your financial objectives, whether it’s building an emergency fund, saving for a major purchase, or simply watching your money grow over time.

Frequently Asked Questions

Are HYSAs safe?

Yes, high-yield savings accounts are generally considered safe, as they are insured by the FDIC (for banks) or the NCUA (for credit unions) up to the legal limit of $250,000 per depositor, per account ownership type, per financial institution.

Should I put all my money in an HYSA?

While high-yield savings accounts can be a great place to grow your money, it’s generally not advisable to keep all of your savings in a single account. Diversification is an important principle of personal finance, so it’s best to distribute your money across different savings and investment vehicles to manage risk.

Do you pay taxes on HYSA interest?

Yes, the interest earned on a high-yield savings account is considered taxable income. You’ll need to report the interest earned on your annual tax return, and it will be subject to federal and potentially state income tax.

Are HYSA rates fixed?

No, the interest rates on high-yield savings accounts are variable, meaning they can change over time. These rates are influenced by the Federal Reserve’s monetary policy decisions and other market conditions.

Can you take money out of an HYSA?

Yes, you can withdraw or transfer money from a high-yield savings account as needed. However, federal regulations limit the number of withdrawals and transfers you can make per month, typically to six. Exceeding this limit may result in fees or the account being converted to a checking account.